With the extend stamp duty holiday in England and Northern Ireland coming to an end on 30th June, what happens next?

Almost a year since this temporary reduction and it has meant no stamp duty tax to pay for first time buyers and home movers purchasing properties below £500,000 before end of June 2021.

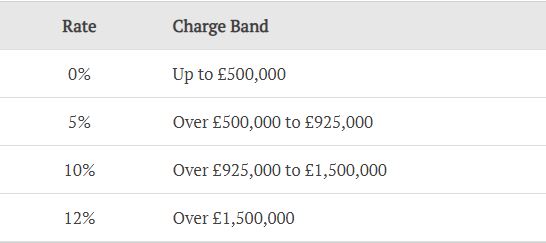

From 1st July, a staggered return will be introduced to previous stamp duty rates. The nil – rate band will be lowered from £500,00 to £250,000 until 30th September. From 1st October 2021 it will return to £125,000.

The rate will also depend on if you’re a first-time buyer. From 1 July, first-time buyers will pay no stamp duty on properties worth up to £300,000, and a discounted rate on properties up to £500,000.

With the stamp duty tax thresholds on property purchases set to change, if you’re thinking of moving soon you can use the stamp duty calculator on rightmove to work out how much you’ll pay.

Thinking of selling your property and have questions that need answering about selling your property? Simply contact one of our branches for help.